- Bank of America leads closures: 168 branches closed in 2024 plus 56 more in 2025, part of a wider nationwide shrinkage.

- Bank says closures reflect a "high-tech, high-touch" shift—investing billions and opening new centers even as many local branches shutter.

- Rising digital banking fuels closures, risking "banking deserts" and disadvantaging seniors, low-income residents, and areas with poor internet.

In a sign of the times for America’s banking landscape, Bank of America is shuttering dozens more branches this year, adding to a tally that already makes it the leader in closures among major financial institutions.

The moves come amid a broader industry trend where physical locations are giving way to apps and online portals, but not without raising eyebrows about access for those who still prefer—or need—a face-to-face transaction.

Bank of America closed 168 branches in 2024, outpacing every other bank, and has followed up with 56 more shutdowns so far in 2025, according to data compiled from federal regulators and news reports.

The FrankNez Media Daily Briefing newsletter provides all the news you need to start your day. Sign up here.

That’s on top of 99 closures the year before, as documented in the bank’s own filings with the Office of the Comptroller of the Currency (OCC).

In the first three months of this year alone, 26 locations across 18 states and Washington, D.C., pulled down the shades—from bustling spots in California and Florida to quieter outposts in Ohio and Pennsylvania.

The latest round includes some high-profile spots.

Come September, doors will lock for good at the 201 Bastogne Avenue branch in Fort Campbell, Kentucky; 1206 South Bowen in Arlington, Texas; and 300 South Fourth Street in Las Vegas, Nevada.

October brings the end for the Savannah Highway location in Charleston, South Carolina, and one in Huntington Beach, California. November hits Camarillo, California, and December claims a site on California Street in San Francisco.

Californians, in particular, are feeling the pinch: The state has seen more than a dozen Bank of America branches close this year, part of a pattern that’s left the Golden State with the highest number of total bank closures over the past decade—1,114 since 2014.

Big Changes Coming to Bank of America

It’s not all downsizing, though. Bank of America insists its strategy is about smart evolution, not retreat.

“Our financial center network is central to our high-tech, high-touch strategy, and gives us a competitive advantage,” a spokesperson told The US Sun.

The bank has pumped more than $5 billion into its branches since 2016, opening about 50 new ones annually over the last decade and expanding into 11 new markets.

Looking ahead, it plans 170 fresh centers in over 60 markets in the coming years, including five new spots in Wisconsin this fall: Milwaukee, Madison, Oak Creek, Sun Prairie, and Greendale.

That’s a nod to growth in underserved areas, even as elsewhere the footprint shrinks.

But the optics of closing branches while hiking pay for remaining staff have some scratching their heads.

Just last month, Bank of America announced a bump in its minimum hourly wage to $25 starting in October—up $10 from $15 in 2018—affecting thousands of full- and part-time workers and pushing full-timers toward $50,000-plus annual salaries.

It’s a positive for employees, sure, but it underscores the human cost of these shifts: Fewer branches mean fewer jobs on the front lines.

A National Trend: Bank Closures Accelerating Across the Board

Bank of America isn’t alone in this. The U.S. is on track for another year of record branch losses, with more than 320 closures announced in the first 13 weeks of 2025 alone, per OCC filings.

In Q1, net closings hit 148—up sharply from 21 in late 2024—according to S&P Global Market Intelligence.

By May, the tally topped 336, and experts warn the pace could top last year’s 1,043 shutdowns by more than 4%.

Big players like Wells Fargo (49 closures flagged for 2025), U.S. Bank (40), Flagstar (52), and JPMorgan Chase are all trimming their maps, with the top five banks axing a net 175 locations in Q3 2024 alone.

The numbers paint a stark picture.

From 2018 to 2022, an average of 1,646 branches vanished yearly, and if that holds, experts from fintech firm Self Financial predict the last physical U.S. bank could shutter by 2041.

States like California (1,080 closures from 2002-2022), Illinois, and Florida top the list for losses, while rural and low-income areas risk turning into “banking deserts”—zones where the nearest branch is miles away, complicating everything from cashing checks to applying for loans.

Holiday timing hasn’t helped public perception, either.

Between Thanksgiving 2024 and early January 2025, over 100 branches nationwide closed quietly, including spots from Bank of America, Wells Fargo, U.S. Bank, and PNC—part of 113 announced in that window, per the Daily Mail.

Critics point to inflation’s bite: Soaring rents, real estate costs, and interest rates are squeezing margins, especially as foot traffic plummets.

The Digital Divide: Convenience for Some, Headache for Others

At the heart of it all is a seismic shift to digital.

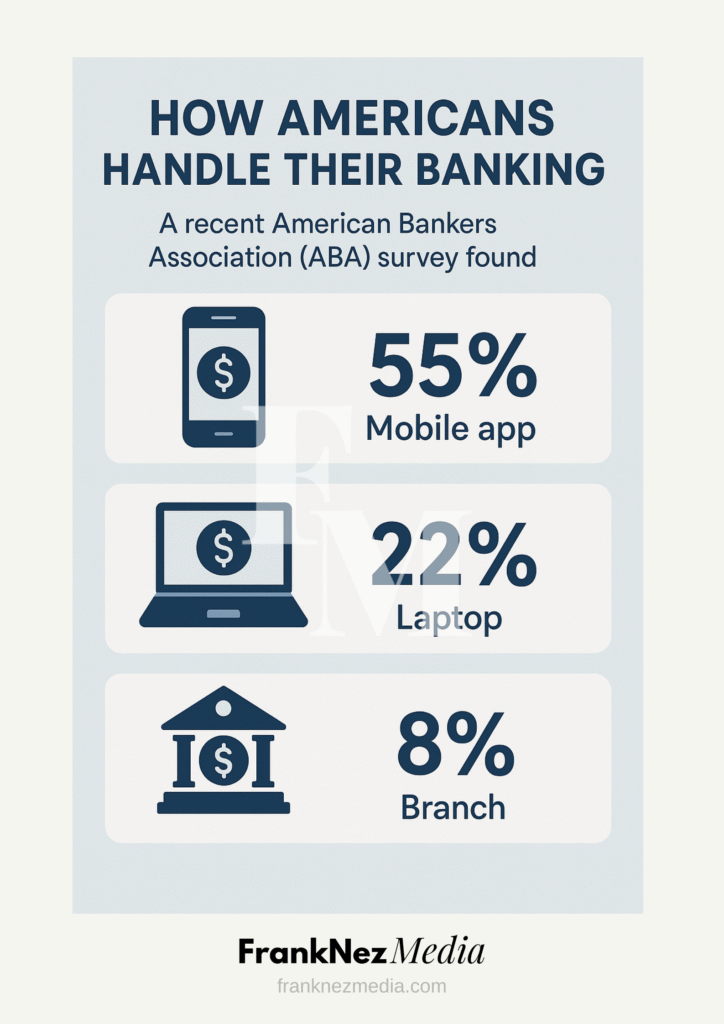

A recent American Bankers Association (ABA) survey found 55% of Americans now handle banking via mobile apps, 22% on laptops, and just 8% at branches—numbers that exploded during COVID and haven’t slowed.

“While the pandemic greatly accelerated mobile banking adoption, America’s banks have sustained—and even increased—this growth by investing in innovative technologies that make banking on-the-go as seamless and secure as ever before,” said ABA Senior Vice President of Innovation Strategy Brooke Ybarra.

She highlighted perks like remote check deposits, instant bill splits, and easy spending trackers as game-changers.

Economist Michael Szanto echoed that in comments to the Daily Mail, stating, “Branch closures are the result of Americans increasingly using online banking instead of in-person transactions. In an increasingly digital paperless economy, the need for physical branches is greatly lessened.”

Statista data backs it up: Only 45% of account holders visited a branch in late 2024, down 8% from mid-2019.

Who Uses Physical Bank Branches the Most?

Baby Boomers still lean on branches the most, while Millennials and Gen Z barely touch them.

But for seniors, low-income folks, or those in spotty internet zones, it’s tougher.

Closures hit job losses—hundreds per wave—and ripple through local economies, turning community hubs into empty storefronts.

One report from the Federal Reserve Bank of Philadelphia flagged how this exacerbates “banking deserts,” especially post-Great Recession and pandemic.

On the flip side, banks argue they’re adapting to demand.

U.S. branches numbered about 77,500 at the start of 2024, down from peaks years ago, with Q3 seeing 439 net closings—the highest in nearly three years.

Mergers could speed things up, too, as consolidation often means overlap and overlaps mean cuts.

What Comes Next for Customers?

If your branch is on the chopping block, options abound: Switch to online banking, hit a nearby alternative, or even change banks if a competitor’s closer.

Tools like the OCC’s weekly bulletins can flag upcoming closures, and apps from the ABA or FDIC track “banking deserts.”

For those sticking with physical, Bank of America’s expansion plans suggest some relief in growing markets.

Still, as one Daily Mail piece put it, these aren’t just numbers—they’re neighborhoods losing anchors.

With digital tools getting smarter (think AI chatbots and “smart” ATMs), the branch era might fade, but the push for equity in access feels more urgent than ever.

Banks like BofA say they’re balancing both worlds, but for now, the map’s getting smaller, one closure at a time.

Also Read: A Massive Convenience Store Now Closes 500 Stores

Google is changing how it surfaces content. Prioritize our high-quality news and industry-leading coverage in search results by setting FrankNez Media as a preferred source.