- Fannie Mae and Freddie Mac raised retained mortgage-backed securities 31% to $233.6 billion, tightening supply and pushing yields down.

- Experts say continued GSE buying plus Fed easing could lower mortgage rates modestly, potentially improving affordability in 2026.

It’s been a tough couple of years for anyone trying to buy a home. Prices are sky-high, and mortgage rates have stayed stubbornly elevated, making that monthly payment feel out of reach for a lot of folks.

But there’s some intriguing news bubbling up that could signal relief ahead.

According to recent reports, Fannie Mae and Freddie Mac—the two government-sponsored giants that back a huge chunk of U.S. mortgages—have been quietly building up their holdings of mortgage-backed securities.

The FrankNez Media Daily Briefing newsletter provides all the news you need to start your day. Sign up here.

– FNM

From May to October 2025, their combined retained portfolio jumped 31 percent, hitting $233.6 billion.

That’s the highest level in four years.

Why does this matter? These entities buy loans from lenders and either keep them or package them into securities for investors.

By holding onto more instead of selling them off quickly, they’re essentially tightening the supply of those securities on the market.

That can drive up prices for the ones that are available, which in turn lowers yields—and that often translates to lower mortgage rates for borrowers.

Experts Weigh In

Experts see this as a deliberate strategy.

Realtor.com senior economist Joel Berner noted: “Fannie and Freddie adding to their balance sheets basically represents a boost in demand for mortgage-backed securities.

This would shift up the price and down the yield on the going market value for home loans, and that depressed yield would equate to lower mortgage rates.”

Vitaliy Liberman, a portfolio manager at DoubleLine Capital, added: “If you want to lower mortgage rates, one of the most direct ways to do so is simply directing the GSEs [Government-Sponsored Enterprises] to purchase more mortgage bonds.

This administration is looking at everything.”

And there’s a political angle here too.

President Donald Trump has been vocal about wanting lower borrowing costs to boost housing affordability.

He’s pushed for Fannie and Freddie to help get big homebuilders moving again.

Back in October, he posted on Truth Social: “Before I became President, ‘OPEC’ kept oil prices high. It wasn’t right for them to do that but, in a different form, is being done again—This time by the Big Homebuilders of our Nation.

They’re my friends, and they’re very important to the SUCCESS of our Country, but now, they can get Financing, and they have to start building Homes.

They’re sitting on 2 Million empty lots, A RECORD. I’m asking Fannie Mae and Freddie Mac to get Big Homebuilders going and, by so doing, help restore the American Dream!”

Trump has also talked about taking Fannie and Freddie public, something he’s given “very serious consideration” to, more than 15 years after they were placed under government conservatorship following the 2008 crisis.

Building up these portfolios could make them more attractive to investors by improving profitability.

A couple signing mortgage documents, representing the challenges and hopes of homebuyers in the current market.

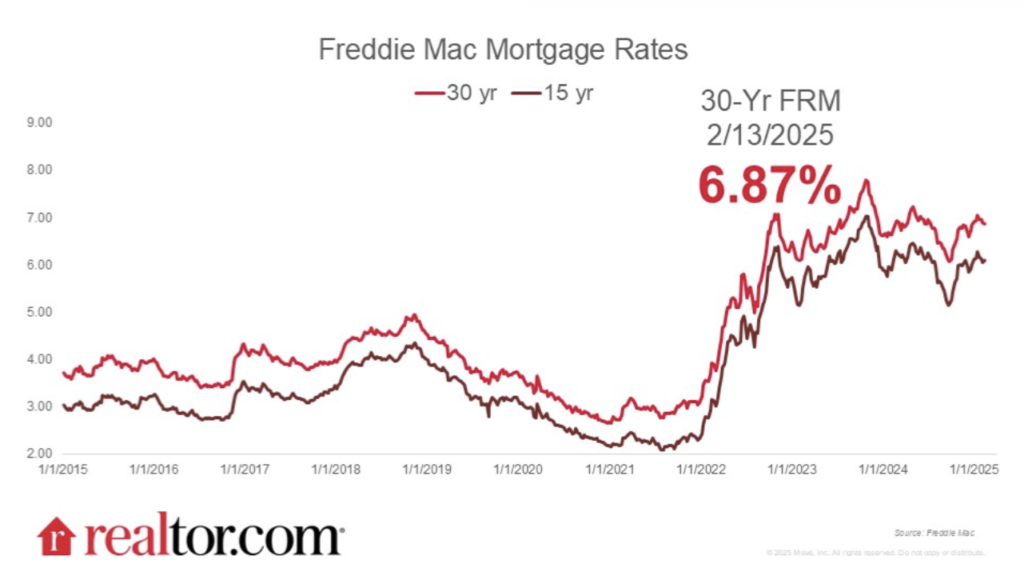

Where Are Mortgage Rates Right Now?

As of mid-December 2025, things are looking a bit more promising than earlier in the year.

Freddie Mac reported that the average 30-year fixed-rate mortgage stood at 6.22% for the week ending December 11—down from 6.60% a year ago, though it ticked up slightly from the prior week.

Other trackers show similar numbers: Bankrate had it around 6.29%, while some daily averages dipped closer to 6%.

The Federal Reserve’s recent rate cuts—three in 2025, including a 25-basis-point reduction in early December—have helped stabilize things after rates hovered in the upper 6% to low 7% range for much of the year.

But rates aren’t crashing dramatically.

The Fed’s moves have been cautious, with officials signaling fewer cuts ahead amid lingering inflation concerns.

Graph of the federal funds rate over time, showing the Federal Reserve’s recent cuts bringing it to 3.5%-3.75%.

Could This GSE Strategy Push Rates Lower?

Analysts think Fannie and Freddie might keep adding to their portfolios—potentially another $100 billion in 2026.

If that’s the case, it could provide direct downward pressure on rates, bypassing some of the usual bond market volatility.

This comes at a time when the housing market could really use a break.

Home sales have been sluggish, inventory is building in some areas, and affordability remains a huge hurdle.

Stubbornly high rates have been a major drag, even as the Fed has eased policy.

President Trump has repeatedly called out the Fed for not cutting sooner or more aggressively.

Lower rates via Fannie and Freddie could deliver some of what he’s been asking for without relying solely on central bank action.

Of course, the companies haven’t officially explained the buildup, and Newsweek said it reached out for comment but hadn’t heard back at the time of the original report.

What Experts Are Saying About 2026

Forecasts vary, but many see modest relief coming.

Fannie Mae has projected rates ending 2026 around 6.1%, with some earlier outlooks dipping lower.

Others, like the Mortgage Bankers Association, are more conservative, expecting averages in the mid-6% range.

If the GSEs continue this approach—and combined with any further Fed easing—it could help nudge rates down enough to bring more buyers off the sidelines.

That might finally thaw the “lock-in effect,” where homeowners with ultra-low rates from a few years ago hesitate to sell and take on higher ones.

For now, though, prospective buyers are still navigating a tricky landscape. Rates around 6.2% are better than the peaks earlier this year, but far from the sub-3% days that feel like ancient history.

If you’re in the market, shopping around lenders and considering points to buy down your rate could make a difference.

And keeping an eye on these behind-the-scenes moves by Fannie and Freddie might just pay off—literally.

For more on updates like this, set FrankNez Media as a preferred source below.

Also Read: Trump’s Latest Executive Order is Now Under Fire by GOP

Contact | About | Home | Newsletter

Google is changing how it surfaces content. Prioritize our high-quality news and industry-leading coverage in search results by setting FrankNez Media as a preferred source.