- FOIA emails reveal "shares on loan" from the FINRA halt cannot be recovered, leaving lenders and investors stuck.

- FINRA halt Dec 9, 2022 prevented shareholders from trading MMTLP right before Next Bridge distribution, causing illiquidity.

- Industry groups warned SEC the proposed S-1 would block reconciliation and harm investor protections and tax treatments.

A recently released batch of internal emails from the U.S. Securities and Exchange Commission (SEC) sheds new light on the operational headaches surrounding Next Bridge Hydrocarbons, Inc., a private oil and gas company born from a controversial spin-off of assets from Meta Materials, Inc.

The documents, obtained via a Freedom of Information Act (FOIA) request, show industry groups raising red flags about the company’s proposed direct-registration process for shareholders — and highlights ‘shares on loan’ which can no longer be recovered.

Next Bridge Hydrocarbons emerged in late 2022 when Meta Materials spun off its oil and gas holdings into a separate entity.

Shareholders in Meta’s Series A Preferred Stock (traded as MMTLP) were to receive Next Bridge common stock in a 1:1 distribution.

But the process hit roadblocks almost immediately from FINRA and alleged bad actors who benefited from this unprecedented fall.

Trading in MMTLP was halted by FINRA on December 9, 2022, just days before the planned distribution, leaving many holders unable to sell or trade their positions.

The halt was justified by FINRA as necessary to “protect investors” — that’s right, freezing investors’ funds and preventing them from pulling out their life savings is how regulators acted.

Prior to these new FOIA findings, emails between the SEC and FINRA surfaced about a fraud investigation that was happening prior to the rare U3 halt.

The following information you are about to read further highlights the negligence retail investors have faced at the mercy of Wall Street regulators.

Financial Information Forum Flags Major Red Flags

The emails, exchanged between SEC staff and representatives from the Financial Information Forum (FIF) — an industry group representing broker-dealers, exchanges, and tech vendors — highlight concerns voiced in 2023.

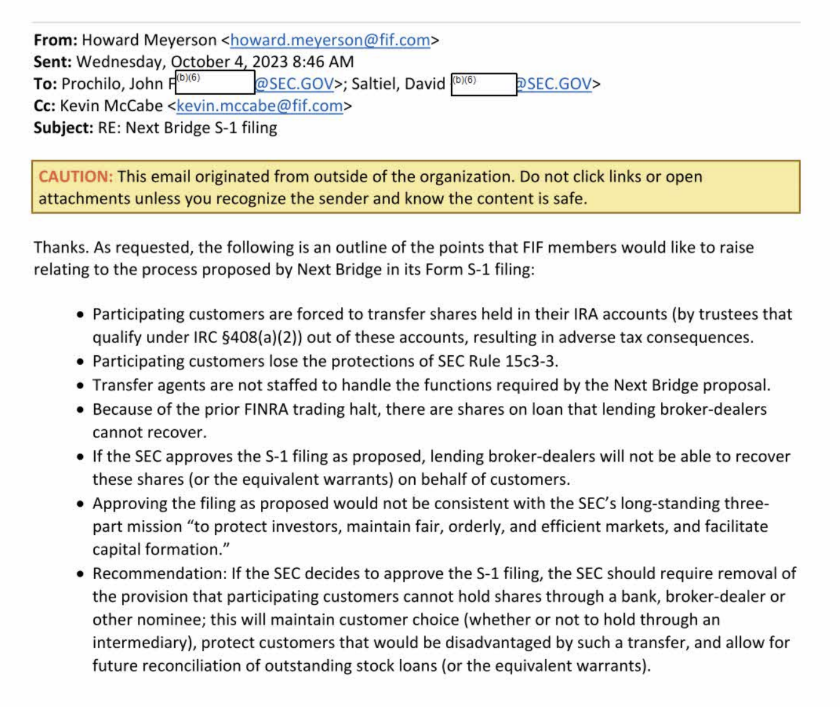

In one exchange dated October 4, 2023, FIF Managing Director Howard Meyerson outlined key objections to Next Bridge’s Form S-1 filing:

- Participating customers are forced to transfer shares held in their IRA accounts (by trustees that qualify under IRC §408(a)(2)) out of these accounts, resulting in adverse tax consequences.

- Participating customers lose the protections of SEC Rule 15c3-3.

- Transfer agents are not staffed to handle the functions required by the Next Bridge proposal.

- Because of the prior FINRA trading halt, there are shares on loan that lending broker-dealers cannot recover.

- If the SEC approves the S-1 filing as proposed, lending broker-dealers will not be able to recover these shares (or the equivalent warrants) on behalf of customers.

- Approving the filing as proposed would not be consistent with the SEC’s long-standing three-part mission “to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation.”

This is the part that has had retail investors calling foul for years.

This FOIA information on shares on loan that have been stuck in limbo is significant for many reasons.

For one, it means this is no longer a retail investor theory. And two, it pressures regulators who need to be held responsible.

FIF also recommended that if the SEC approved the filing, it should remove the provision barring shareholders from holding shares through a bank, broker-dealer, or nominee at the time.

This, they argued, would preserve investor choice and allow reconciliation of outstanding loans.

The emails also reveal follow-up questions from SEC staffer David Saltiel, including inquiries about the transfer agent (identified as AST/Equiniti) and FINRA contacts handling paper certificate distributions.

No specific FINRA names were provided, according to the correspondence.

The self-regulatory body has been scrutinized by retail investors following the halt and been accused of overreach, potentially collaborating with bad actors.

The Naked Short Selling Shadow Over MMTLP and Next Bridge

The MMTLP halt and the Next Bridge distribution have fueled persistent allegations of naked short selling — selling shares without borrowing them first, potentially creating “counterfeit” shares that exceed the actual float.

Retail investors, many active on social media platforms like X and Reddit, have long claimed that excessive short interest in MMTLP led to more shares being traded than legally existed.

Investors argue the halt trapped legitimate shares while allowing short positions to be “forced” into Next Bridge without resolution, with some alleging sellers profited prior to the halt as a coordinated attack.

Investors had to register shares directly with AST to qualify for future distributions or benefits, but many have reported difficulties transferring from brokers throughout the years.

As of mid-2025, Next Bridge remains a private company with no public trading market, leaving shareholders illiquid and frustrated.

Ongoing SEC Scrutiny and Company Updates

And with MMTLP now 3 years deep without resolution, you bet a sleeping giant is waking up soon.

The question now that these emails have gone public is, what will regulators do next?

Will they respond to the negligence, or will they continue to kick the can down the road.

One thing is certain — retail investors aren’t going anywhere without a fair fight.

Independent media is under attack by industry policies, set FrankNez Media as a preferred source below to fight against media suppression.

Also Read: A Hedge Fund Now Announces an Unexpected Closure

Contact | About | Home | Newsletter

Google is changing how it surfaces content. Prioritize our high-quality news and industry-leading coverage in search results by setting FrankNez Media as a preferred source.